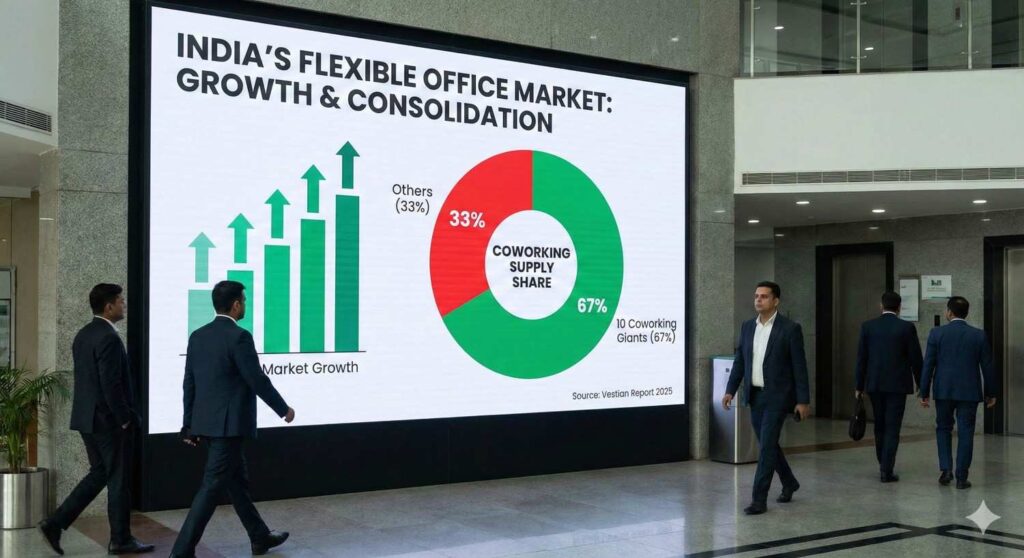

India’s flexible workspace sector is expanding rapidly but remains highly consolidated. A Vestian report reveals that 10 major coworking operators control 67% of the 82 million sq ft flex office stock across top cities. Rising GCC demand is accelerating growth, with total stock expected to cross 100 million sq ft by 2026.

India’s coworking and flexible office market has reached a significant milestone, with total stock touching 82.3 million square feet across nearly 1,400 centres in the country’s top seven cities. However, growth has not been evenly distributed. According to a recent Vestian report, the top 10 flexible workspace operators now control 67% of the total supply, highlighting a highly consolidated market. This dominance underscores how scale, capital strength, and enterprise readiness are increasingly defining success in the flex space segment.

GCC Demand Driving Flexible Workspace Adoption

One of the strongest demand drivers for flexible offices remains Global Capability Centres (GCCs). Vestian Research estimates that India is home to over 1,750 GCC companies operating through nearly 3,800 centres. Over the past two years, GCCs have accounted for more than 40% of total office space demand, reflecting their growing reliance on India as a global operations hub.

“As India’s GCC landscape continues to evolve, flexible space operators will remain indispensable partners, offering flexibility, faster speed to market, and enterprise-grade infrastructure that global companies require, to scale efficiently in a highly competitive market,” said Shrinivas Rao, CEO of Vestian.

Where the Supply Is Concentrated

Bengaluru continues to lead India’s flexible workspace market, holding 33.2% of the total stock. Delhi-NCR follows with a 20.4% share, while Pune accounts for 14.7%. Hyderabad has emerged as another strong flex office hub, with 12.4% growth, supported by steady technology and GCC-led demand. Mumbai, Chennai, and Kolkata contribute 9.2%, 8.5%, and 1.6%, respectively. This distribution reflects both corporate occupier preferences and the maturity of local commercial real estate ecosystems.

Coworking Operators as Strategic Partners

To capitalise on sustained demand, coworking operators are increasingly positioning themselves as long-term strategic partners rather than short-term space providers. Vestian notes that more than 475 of the 1,400 flexible workspace centres across Tier-1 cities currently host GCC operations. This shift is pushing operators to upgrade infrastructure, enhance compliance standards, and offer customised enterprise solutions that align with global occupier expectations.

What Lies Ahead for the Flex Space Sector

Despite the current consolidation, the sector’s growth trajectory remains strong. Vestian projects that India’s flexible workspace stock will exceed 100 million square feet across Tier-1 cities by 2026. While the report does not name the top 10 operators, several large players—including WeWork India, Smartworks, Awfis, and IndiQube Spaces—are already publicly listed, while others like The Executive Centre, Incuspaze, Table Space, and BHIVE Workspace continue to expand aggressively. As enterprise demand deepens, scale and service depth are likely to further separate market leaders from smaller players.